Archive for the ‘recode’ Category

Africa’s Mobile-Sun Revolution

Solar panels are a part of the landscape in southern Africa. Here, two boys ham it up for the camera while playing around a large-form factor panel.

The transformative potential for mobile communications is upon us in every aspect of life. In the developing world where infrastructure of all types is at a premium, few question the potential for mobile, but many wonder whether it should be a priority.

Note: This post originally appeared in Re/code on April 29, 2015.

Many years of visiting the developing world have taught me that, given the tools, people — including the very poor — will quickly and easily put them to uses that exceed even the well-intentioned ideas of the developed world. Poor people want to and can do everything people of means can do, they just don’t have the money.

Previously, I’ve written about the rise of ubiquitous mobile payments across Africa, and the work to bring free high-speed Wi-Fi to the settlements of South Africa. One thing has been missing, though, and that is access to reliable sources of power to keep these mobile phones and tablets running. In just a short time — less than a year — solar panels have become a commonplace site in one relatively poor village I recently returned to. I think this is a trend worth noting.

Could it be that solar power, potentially combined with large-scale batteries, will be the “grid” in developing markets, perhaps in the near future? I think so.

It is also the sort of disruptive trend we are getting used to seeing in developing markets. The market need and context leads to solutions that leapfrog what we created over many years in the developed world. Wireless phones skipped over landlines. Smartphones skipped over the PC. Mobile banking skipped over plastic cards and banks.

Could it be that solar power, potentially combined with large-scale batteries, will be the “grid” in developing markets, perhaps at least in the near future? I think so. At the very least, solar will prove enormously useful and beneficial and require effectively zero-dollar investments in infrastructure to dramatically improve lives. Solar combined with small-scale appliances, starting with mobile phones, provides an enormous increase in standard of living.

Infrastructure history

Historically, being poor in a developing economy put you at the end of a long chain of government and international NGO assistance when it comes to infrastructure. While people can pull together the makings of shelter and food along with subsistence labor or farming, access to what we in the developing world consider basic rights continues to be a remarkable challenge.

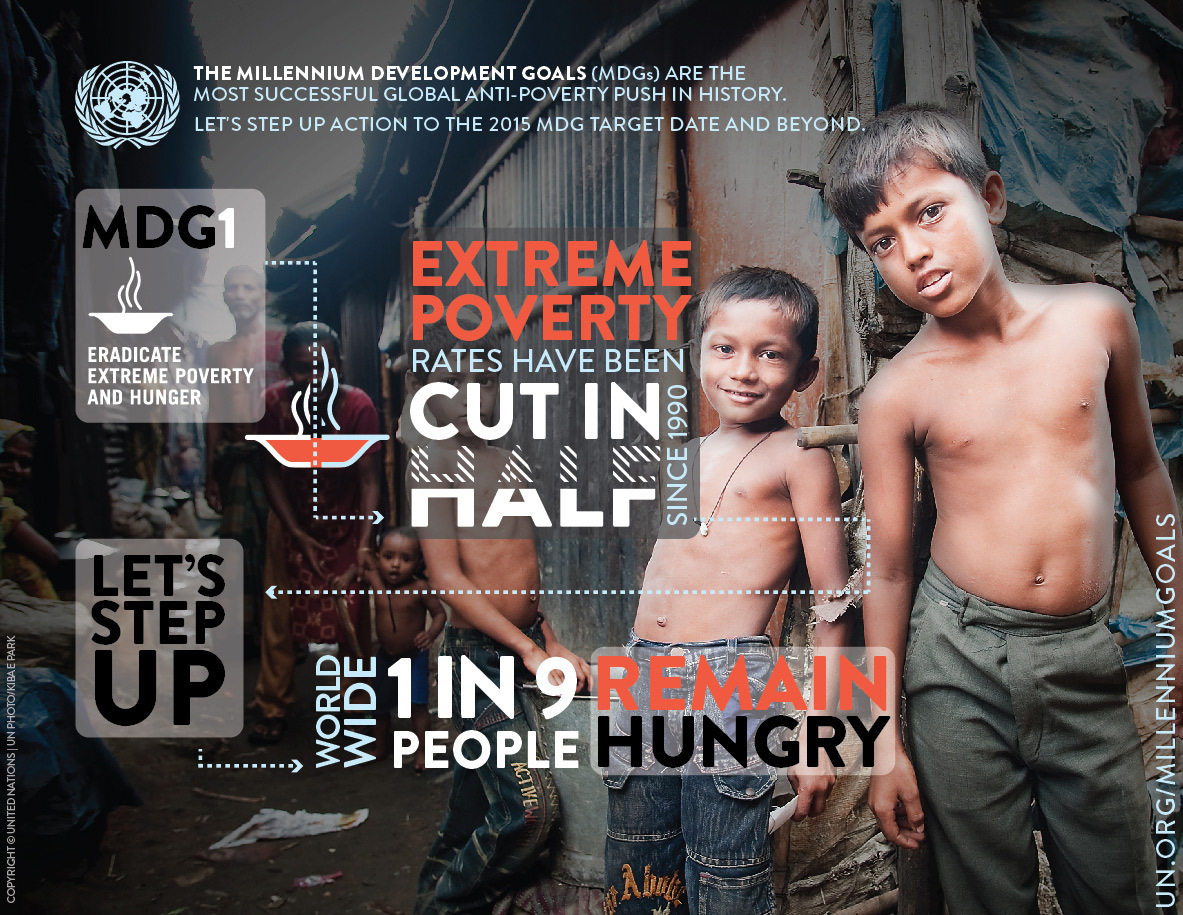

For the past 50 or more years, global organizations have been orchestrating “top down” approaches to building infrastructure: Roads, water, sewage and housing. There have been convincing successes in many of these areas. The recent UN Millennium Development Goals report demonstrates that the percentage of humans living at extreme poverty has decreased by almost half. In 1990, almost half the population in developing regions lived on less than $1.25 a day, the common definition of extreme poverty. This rate dropped to 22 percent by 2010, reducing the number of people living in extreme poverty by 700 million.

Nevertheless, billions of people live every day without access to basic infrastructure needs. Yet they continue to thrive, grow and improve their lives.

This UN Millennium Development Goals infographic shows the dramatic decline in percentage of people living under extreme poverty. (United Nations)

While the efforts to introduce major infrastructure will continue, the pace can sometimes be slower than either the people would like or what those of us in the developing world believe should be “acceptable.”

A village I know of, about 10 miles outside a major city in southern Africa, started from a patch of land contributed by the government about six years ago, and grew to a thriving neighborhood of 400 single-family homes. These homes are multi-room, secure, cement structures with indoor connections to sewage. The families of these homes earn about $100-$200 a month in a wide range of jobs. By way of comparison, these homes cost under $10,000 to build.

While the roads are unpaved, this is hardly noticed. But one thing has become much more noticeable of late is the lack of electrical power. Historically, this has not been nearly as problematic as we in the developing world might think. Their economy and jobs were tuned to daylight hours and work that made use of the energy sources available.

Solar-powered streetlights have been installed recently — here under construction — increasing public safety and providing light to the community.

Several finished homes around a nearly complete streetlight installation that also illuminates a drinking-water well, enabling nighttime access to water.

In an effort to bring additional safety to the village, the citizens worked with local government to install solar “street lights,” such as the one pictured here. This simple development began to change the nighttime for residents. These were installed beginning about nine months ago (as seen in the first photo, with a closer to production installation in the second).

Historically, this type of infrastructure, street lighting, would come after a connection to the electrical grid and development of roads. Solar power has made this “reordering” possible and welcome. Lighting streets is great, but that leads to more demands for power.

Mobile phones, the new infrastructure

These residents are pretty well off, even on relatively low wages that are three to five times the extreme poverty level. While they lack electricity and roads, they are safe, secured and sheltered.

One of the contributors to the improved standard of living has been mobile phones. Over the past couple of years, mobile phone penetration in this village has reached essentially 100 percent per household, and most adults have a mobile.

The use of mobiles is not a luxury, but essential to daily life. Those that commute into the city to sell or buy supplies can check on potential or availability via mobile.

Families can stay connected even when one goes far away for a good job or better work. Safety can be maintained by a “neighborhood watch” system powered by mobile. Students can access additional resources or teacher help via mobile. Of course, people love to use their phones to access the latest World Cup soccer results or listen to religious broadcasts.

All of these uses and infinitely more were developed in a truly bottom-up approach. There were no courses, no tutorials, no NGOs showing up to “deploy” phones or to train people. Access to the tools of communication and information as a platform were put to uses that surprise even the most tech-savvy (i.e., me). Mobile is so beneficial and so easy to access that it has quickly become ubiquitous and essential.

Last year, when I wrote for Re/code about mobile banking and free Wi-Fi, I received a fair number of comments and emails saying how this seemed like an unnecessary luxury, and that smartphones were being pushed on people who couldn’t afford the minutes or kilobytes, or would much rather have better access to water or toilets. The truth is, when you talk to people who live here, the priority for access unquestionably goes to mobile communication. In their own words, time and time again, the priority is attached to mobile communications and information.

Fortunately, because of the openness most governments have had to investments from multinational telecoms such as MTN, Airtel and Orange, most cities and suburban areas of the continent are well covered by 2G and often 3G connectivity. The rates are competitive across carriers, and many people carry multiple SIMs to arbitrage those rates, since saving pennies matters (calls within a carrier network are often cheaper than across carriers).

Mobile powered by solar

There has been one problem, though, and that is keeping phones charged. The more people use their phones (day and night), the more this has become a problem. While many of us spend time searching for outlets, what do you do when the nearest outlet might be a few miles away?

It is not uncommon to see one outlet shared by many members of a community. This outlet is in the community center, which is one of a small number of grid-connected structures. Note the variety of feature phones.

When there is an outlet, you often see people grouped around it, or one person volunteers to rotate phones through the charging cycles. Above a picture of an outlet in the one building connected to power, the community center. This is a pretty common sight.

Small portable solar panels can serve as “permanent” power sources when roof-mounted. You can see the extension wire drawn through the window.

An amazing transformation is taking place, and that is the rise of solar. What we might see as an exotic or luxury form of power for hikers and backpackers, or something reasonably well-off people use to augment their home power, has become as common a sight as the water pump.

The plethora of phones sharing a single outlet has been replaced by the portable solar panel out in front of every single home.

An interesting confluence of two factors has brought solar so quickly and cheaply to these people. First, as we all know, China has been investing massively in solar technology, solar panels and solar-powered devices. That has brought choice and low prices, as one would expect. In seeking growth opportunities, Chinese companies are looking to the vast market opportunity in Africa, where people are still not connected to a grid. There’s a full supply chain of innovation, from the solar through to integrated appliances with batteries.

Second, China has a significant presence in many African countries, and is contributing a massive amount of support in dollars and people to build out more traditional infrastructure, particularly transportation. In fact, many Chinese immigrants in country on work projects become the first customers of some of these solar innovations.

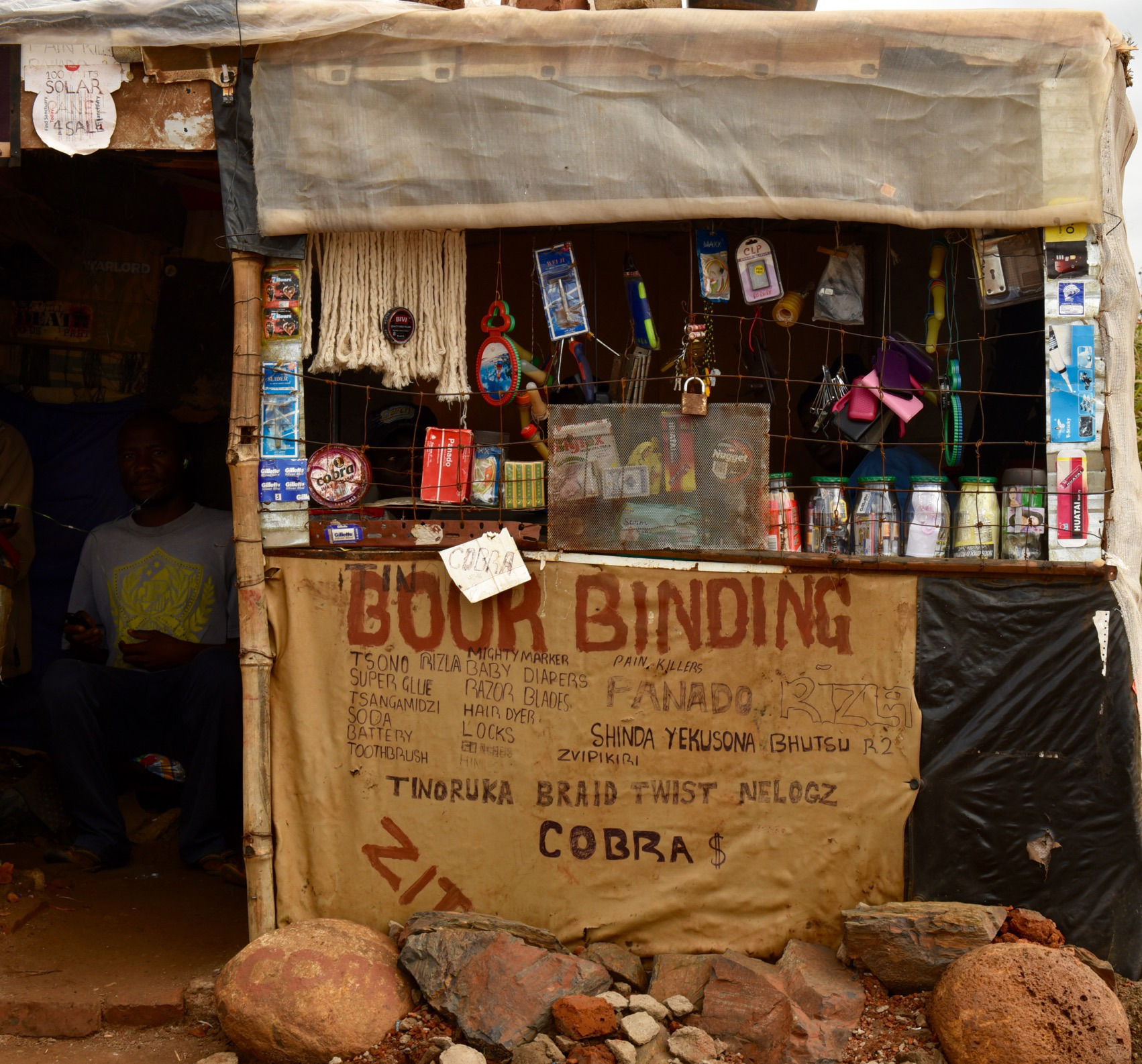

People are exposed to low-cost, low-power portable solar panels and they are “hooked.” In fact, you can now see many small stores that sell 100w panels for the basics of charging phones. You can see solar for sale in the image below. I left the whole store in the photo just to offer a bit of culture. The second photo shows the solar “for sale” offers.

A typical storefront in this community, selling a variety of important products for the home. Solar panels are for sale, as indicated by the signs in the upper left.

Detail from the storefront showing the solar panels for sale. There is a vibrant after-market for panels, as they often change hands, depending on the capital needs of a family.

Like many significant investments, there’s a vibrant market in both used panels and in the repair and maintenance of panels and wiring. Solar is a budding industry, for sure.

But people want more than to charge their phones once they see the “power” of solar. Here is where the ever-improving and shrinking of solar, LED lights, lithium batteries and more are coming together to transform the power consumption landscape and the very definition of “home appliances.”

In the developed world, we are transitioning from incandescent and fluorescent lighting in a rapid pace (in California, new construction effectively requires LED). LED lights, in addition to lasting “forever,” also consume 80 percent less power. Combining LED lights, low-cost rechargeable batteries and solar, you can all of a sudden light up a home at night. Econet is one of the largest mobile carriers/companies in Africa, and has many other ventures that improve the lives of people.

Here are a few Econet-developed LED lanterns recharging outside a home. This person has three lights, and shares or rents them with neighbors as a business. Not only are these cheaper and more durable than a fossil-fuel-based lantern, they have no ongoing cost, since they are powered by the sun.

Several modern, portable, solar-powered LED lamps sold at very low cost by mobile provider Econet. The owner rents these lamps out for short-term use.

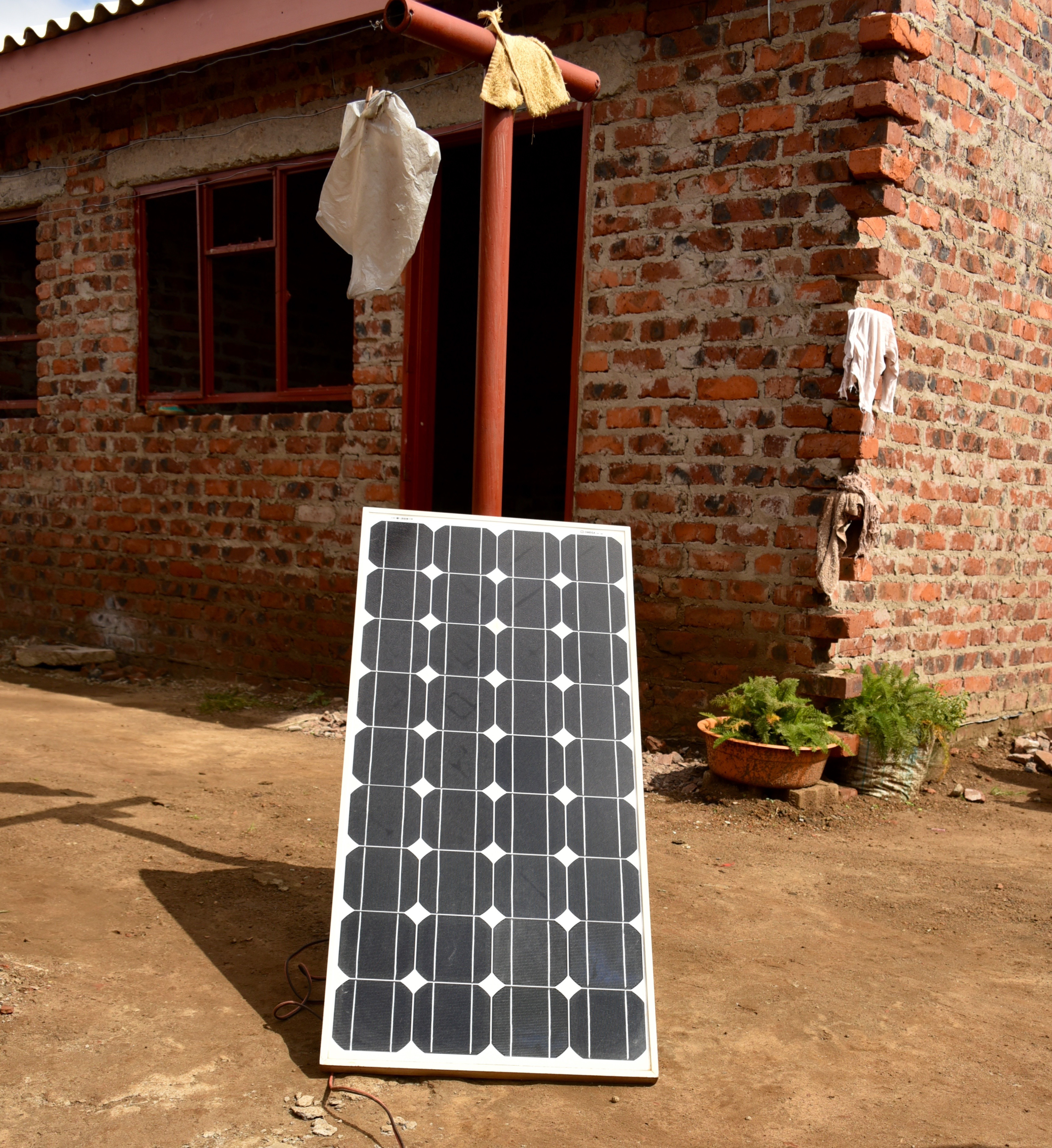

With China bringing down the cost of larger panels, and the abundance of trade between Africa and China, there’s an explosion in slightly larger solar panels. In fact, many of the homes I saw just nine months ago now commonly sport a large two-by-four-foot solar panel on the roof or strategically positioned for maximal use.

These two boys were hanging out when I walked by, and quickly chose a formal pose in front of their home, which has a large permanent solar panel mounted on the roof.

Panels are often on the ground, because they move between homes where the investment for the panel has been shared by a couple of families. This might seem inefficient or odd to many, but the developing world is the master of the shared economy. Many might be familiar with the founding story of Lyft based on experiences with shared van rides in Zimbabwe, Zimride.

A trio of medium-sized solar panels strategically placed outside the doors of several homes sharing a courtyard.

Just the first step

We are just at the start of this next revolution at improving the lives of people in developing economies using solar power.

Three sets of advances will contribute to improved standards of living relative to economics, safety and comfort.

First, more and more battery-operated appliances will make their way into the world marketplace. At CES this year, we saw battery-operated developed-market products for everything from vacuum cleaners to stoves. Once something is battery-powered, it can be easily charged. These innovations will make their way to appliances that are useful in the context of the developing world, as we have seen with home lighting. The improvement in batteries in both cost and capacity (and weight) will drive major changes in appliances across all markets.

Second, the lowering of the price of solar panels will continue, and they will become commonplace as the next infrastructure requirement. This will then make possible all sorts of improvements in schools, work and safety. One thing that can then happen is an improvement in communication that comes from high speed Wi-Fi throughout villages like the one described here. Solar can power point-to-point connectivity or even a satellite uplink. Obviously, costs of connectivity itself will be something to deal with, but we’ve already seen how people adapt their needs and use of cash flow when something provides an extremely high benefit. It is far more likely that Wi-Fi will be built out before broad-based 3G or 4G coverage and upgrades can happen.

Third, I would not be surprised to see innovations in battery storage make their way to the developing markets long before they are ubiquitous in the developed markets.

A full-sized “roof” solar panel leaning up against a clothesline. Often roof-mounting panels is structurally challenging, so it is not uncommon to see these larger panels placed nearby on the ground.

Developed markets will value batteries for power backup in case of a loss of power and solar storage (rather than feeding back to the grid). But in the developing markets, a battery pack could provide continuous and on-demand power for a home in quantity, as well as nighttime power allowing for studying, businesses and more. This is transformative, as people can then begin to operate outside of daylight hours and to use a broader range of appliances that can save time, increase safety in the home and improve quality of life.

Our industry is all about mobile and cloud. With the arrival of low-cost solar, it’s no surprise that the revolution taking place in developing markets these days is rooted in mobile-sun.

Photos by the author unless otherwise noted.

Essay: Workplace Trends, Choices and Technologies for 2015

What’s in store for 2015 when it comes to technology advances in the workplace?

What’s in store for 2015 when it comes to technology advances in the workplace?

Originally appeared on <re/code> December 18, 2014.

This next year will see these technologies broadly deployed, but with that deployment will come challenges and choices to make. This sets up 2015 to be a year of intense activity and important choices — how far forward to leap, and how to transition from a world we all know and are working in comfortably. In today’s context of the primacy of smartphone and tablet devices, robust cross-organization cloud services and the changing nature of productivity — all combined with the acute needs of enterprise security — lead to dramatic change in the definition of the enterprise computing platform, starting this year.

Amazing 2014

This past year has seen an incredible — and exponential — diffusion of technologies. Who would have thought at the start of the year we would end the year surrounded by:

- Smartphone/supercomputers, some costing less than $50 contract-free, in the hands of almost two billion people

- Free (essentially) or unlimited cloud storage for individuals and businesses

- Tablets outselling laptops

- 4G LTE speeds from a single worldwide device in most of the developed world

- Amazing pixel densities on large-screen displays, introduced without a premium price

- Streaming 4K video

- Apple’s iPhone 6 Plus “phablet” sold very well (we think) and is now perfectly normal to use

- SaaS/cloud services scaling to tens of millions of business subscribers

- Major cloud platforms putting millions of servers in their data centers

- Shared transportation is on a path to substitute for traditional taxis, and in many cases, private car ownership

- Mobile payments finally arrived at scale in the U.S. and are routine in some of the world’s least developed economies

These and many more advances went from introduction to deployment, especially among technology leaders and early adopters, thus creating a “new normal.” In terms of Geoffrey Moore’s seminal work from 1991, “Crossing the Chasm,” these technologies have been adopted by technical visionaries and are now crossing the chasm to the broader population.

In the real™ world, technology diffusion takes time (deployment, change, etc.), so we have not yet seen the full impact of any of the above. Moving forward to that future — not just making changes for the sake of change — requires a point of view and making trade-offs. This post has in mind the pragmatists (in Moore’s terminology) who want to accelerate and get the benefits from technology transition. Early visionary adopters have already made their moves. Pragmatists often face the real work in bringing the technology to the next stage of adoption, but often also face their own tendency toward skepticism of step-function changes, along with trade-offs in how to move forward.

Viewpoint 2015

Even with many hard choices and challenges, for me, the coming year is a year of extreme optimism for what will be accomplished and how big a difference a year will make. Looking at the directions firmly seeded in 2014, the following represent strategies and choices for 2015 that demand an execution-oriented point of view:

- Enterprise cloud comes to everyone

- Email isn’t dead, just wounded, but kill off attachments with prejudice

- Productivity breaks from legacy work products and workflows

- Tablets make a “surprise comeback”

- Mobile device management aims to get it right

- Hybrid cloud ROI isn’t there, and the complexity is huge

- Cross-platform really (still) won’t work

- Massive security breaches challenge the enterprise platform

Enterprise cloud comes to everyone.

When it comes to cloud services for typical information workflows, bottom-up adoption, enterprise pilots and trials defined 2014. The debate over on-premise versus cloud will mostly fade as the pragmatists see that legacy “on-prem” or hosted on-prem software can no longer innovate fast enough or connect to the wide array of services available. Cloud architecture is different, and new software is required to benefit from moving to the cloud. The defensibility of holding an enterprise back or attempts to find plug-replacements for existing legacy systems proved weak, and the demand from business unit leaders and employees for mobile access, cross-product integration, enterprise-spanning collaboration and the inherent flexibility of cloud architecture is too great.

The most substantial development in 2015 will be enterprises defaulting to multi-tenant, public-cloud solutions recognizing that the perceived risks or performance and scale challenges are far less than any existing on-prem or hosted solution or upgrade of the same. The biggest drivers will prove to be the need for primarily mobile access, cross-enterprise collaboration and even security. The biggest risk will be enterprises that continue to shut off or regulate access to solutions, especially by preventing use of enterprise email credentials or devices.

The biggest enterprise opportunity will be integrating leading offerings with enterprise sign-on and namespace to permit easy bottom-up usage across the enterprise, with minimal friction. Because of the rapid switch to cloud, we will see legacy on-prem providers relabel or rebrand hosted legacy solutions as cloud. The attributes of cloud “native” will be key purchase criteria, more than legacy compatibility.

Email isn’t dead — just wounded — but kill off attachments with prejudice.

So much has been said and written about the negatives of email and the need for it to go away. Yet it keeps coming back. The truth is, it never went away, but it is changing dramatically in how it is used. Anyone that interacts with millennials knows that email is viewed the way Gen-Xers might view a written letter, as an overly formal means of communication. Long threads, attachments and elaborate formatting are archaic, confusing and counter to collaboration. Messaging services and apps trump email for all but the most formal or regulated communication, with no single service dominant, as context matters. In emerging markets, email will never attain the same status as developed markets. Today, receiving links to documents is still suboptimal, with gaps to be closed and features to be created, but that should not slow progress this year.

Using cloud-based documents supports an organization knowing where the single, true copy resides, without concern that the asset will proliferate. Mobile devices can use more secure viewers to see, print and annotate documents, without making copies unnecessarily. The idea of having a local copy of attachments (or mail), or even just an inbox of attachments, is proving to be a security nightmare. Out of that reality, many startups are providing incredibly innovative scaleable solutions that can be deployed now based on using cloud solutions,.

Services like DocSend can track usage of high-value documents. Textio can analyze cloud-based documents without having to extract them from a mail store, or try to locate them on file shares. Quip edits documents and basic spreadsheets, and integrates contextual messaging avoiding both mail and attachments while safely spanning org boundaries.

This year, casting technologies will allow links to be sent to displays via cloud services for documents, as video is today. The leading enterprises will rapidly move away from managing a sea of attachments and collaborating in endless email threads. The cultural change is significant and not to be underestimated, but the benefits are now tangible and needed, and solutions exist. The opportunity for new solutions from startups continues this year, with deployments going big. Save email for introduction, announcements and other one-to-many communications.

Productivity breaks from legacy work products and workflows.

The gold standard for creating business work products is not going anywhere this year, or for 10 more years. The gold standard for business work products, however, is rapidly changing. Nothing will ever be better than Office at creating Office work products. What has significantly changed, in part driven by mobile and in part driven by a generational change in communication approach, is the very definition of work products that matter the most. Gone are the days where the enterprise productivity ninja was the person who could make the richest document or presentation. The workflow of static information, in large, report-based documents making endless rounds as attachments, is looking more and more like a Selectric-created report stuffed in an interoffice envelope.

Today’s enterprise productivity ninja is someone who can get answers on their tablet while on a conference call from an offsite. They focus their energy on the cloud-based tools that have the most up-to-date data, and they get the answers and don’t fret about presentation. They share quickly knowing that content matters more than presentation because of the ephemeral nature of business information. The opportunity for the enterprise is on the back end, and moving to real-time, cloud-based solutions that forgo the traditional delays and laborious ETL efforts of dragging massive amounts of data onto client PCs for analysis. The risk is in seeing cloud solutions as anything but the definitive source of data and as workgroup or side solutions, so integrating with the primary sources of transaction data will provide a great opportunity to the organization.

Tablets make a “surprise comeback”

Some thought 2014 was the year tablets faded. Many debated the long replacement cycle or weak competitive position of tablet between phablet and laptop. The reality is that tablets will outsell laptops this year. Some discount all the cheap Android tablets barely used at home, but then one must discount the laptops that go unused in analogous scenarios. Regardless, one thing distinguished 2014 with respect to tablets, defined as iPads: You see them in the hands of business people everywhere, from the coffee shop to the airport to the conference to the boardroom. On those iPads, there are enterprise apps, email and browsing (and now Office), doing enterprise work.

The big change in 2015 will be (and I am guessing like everyone else) the introduction of a new iPad, and likely first-party keyboard attachments and/or (at least) iOS software enhancements for improved “productivity.” A tablet properly defined is not just a form factor, but is a hardware platform (ARM) and a modern/mobile operating system (iOS, Android, Windows Phone/Windows on ARM). Those characteristics, being a big phone, come with the attributes of security, reliability, performance, connectivity, robustness, app store, thinness, light weight; and above all, those attributes remain constant over time.

Laptops will have their place for another decade or more, but they will become stationary desktop tools used for profession-defining tools (Excel in finance, Photoshop in design, AutoCAD in architecture, and many more). Work will happen first on mobile platforms, for both team agility and organizational security. The scenario that will resonate will be a larger-screened modern-OS tablet with a keyboard and a phone/phablet as a second screen used in concert, as shown by Apple’s Continuity. The most significant opportunity for those making apps will be to design tablet- and phablet-optimized experiences and assume the app is the primary use case.

Mobile device management aims to get it right.

From the enterprise IT perspective, the transition from managing PCs to managing mobile devices (phones and tablets) is both a blessing and a curse. The faster that IT can get out of managing PCs, the better. The core challenge is that in the modern threat environment, it has become essentially impossible to maintain the integrity of a PC over time. Technical challenges, or even impossibility, mean that 2015 could literally see pressure to reduce PCs in use.

If you doubt this, consider the Sony breach and the potential impact it will have on the view of traditionally architected computing. The rise of tablets for productivity is, therefore, a blessing. Over time, any device in widespread use is eventually a target. Therefore, mobile presents the same risk as the bad actors find new techniques to exploit mobile. The curse, and therefore the opportunity, is that our industry has not yet created the right model for mobile device management. We have MDM, sandboxing and user profiles. All of these are so far not entirely well-received by users, and most IT feels they are not yet there, but for the wrong reasons. IT should not feel the need to reintroduce the PC approach to device security (stateful, log-on scripts, arbitrary code inserted all over the device, etc.).

This leads to a lot of opportunity in a critical area for 2015. First, a golden rule is required: Do not impact the performance (battery life, connectivity) or usability of the device. It isn’t more secure for the company to issue two phones — one the person wants to use, and the other they have to use. Like any such solution, people will simply work around the limitation or postpone work as long as possible. This dynamic is what causes people to travel with iPads and leave the laptop at home (along with weight, chargers, two-factor readers and more).

The best bet is to avoid using or emphasizing management solutions that work better on Android, simply because Android allows more hooks and invasive software in the OS. That’s quite typical in the broad MDM/security space right now and is quite counterintuitive. The existence of this level of flexibility enabling more control is itself a potential for security challenges, and the invasive approach to management will almost certainly impact performance, compatibility and usability just as such solutions have on PCs. As tempting as it is, it is neither viable nor more secure long term. Many are frustrated by the lack of iOS “management,” yet at the same time one would be hard-pressed to argue that the full Android stack is more secure. There will be an explosion in enterprise-managed mobile devices this year, especially as tablets are deployed to replace PCs in scenarios, and with that, a big opportunity for startups to get mobile management right.

Hybrid cloud ROI isn’t there, and the complexity is huge.

In times of great change, pragmatists eager to adopt technologies crossing the chasm may choose to seek solutions that bridge the old and new ways of doing things. For cloud computing, the two methods seeing a lot of attention are to virtualize an existing data center, or to architect what is known as a hybrid cloud or hybrid public/private (some mixture of data center and cloud).

History clearly shows that betting on bridge solutions is the fastest way to slow down your efforts and build technical debt that reduces ROI in both the short- and long-term. The reason should be apparent, which is that the architecture that represents the new solution is substantially different — so different, in fact, that to connect old and new means your architectural and engineering efforts will be spent on the seam rather than the functionality. There’s an incredibly strong desire to get more out of existing investments or to find rationale for requiring use of existing implementations, but practically speaking, efforts in that direction will feel good for a short while, and then will leave the product or organization further behind.

As an enterprise, the pragmatic thing to do is go public cloud and operate existing infrastructure as legacy, without trying to sprinkle cloud on it or spend energy trying to deeply integrate with a cloud solution. The transition to client-server, GUI or Web all provide ample evidence in failed bridge solutions, a long tail of “wish we hadn’t done that” and few successes worth the effort. As a startup, it will be tempting to work to land customers who will pay you to be a bridge, but that will only serve to keep you behind your competitors who are skipping a hybrid solution. This is a big bet to make in 2015, and one that will be the subject of many debates.

Cross-platform really (still) won’t work.

It has been quite a year for those who had to decide whether to build for iOS first or Android first. At the start of 2014, the conventional wisdom shifted to “Android First,” though this never got beyond a discussion with most startups. With the release of Android “L” and iOS 8, the divergence in platform strategy is clear, and that reinforced my view of the downsides of cross-platform. My view was, and remains, that cross-platform is a losing proposition. It has really never worked in our industry except as an objection-handler. Even today, almost no software is a reasonable combination of cross-platform, consistent with the native platform, and equally “good” across platforms.

As we start 2015 it is abundantly clear that the right approach is to focus on platform optimized/exploitive apps, leading with iOS and with a parallel and synchronized team on Android. Android fragmentation is technically real, but lost in the debate is the reality that the highly fragmented low-end phones also almost never acquire apps nor do they represent the full Google stack of platform services. So the strategy is to focus on flagship Android, such as Nexus, Samsung and Moto (though one must note that the delay there of “L” was more than a month even on Moto) or to focus on a distribution of Android from a specific OEM that has some critical mass, and is aimed at customers who will actively acquire apps.

To be clear, we are in a fully sustainable two-ecosystem world. But given the current state of engagement, platform readiness and devices, 2015 will see innovation first and best on iOS. If you’re building your app and working on core code to share, one should be cautious how that goal ends up defining your engineering strategy. Typically, once core code is in place, it selects for tools and languages as well as overall abstractions, and what system services are used. These have a tendency to block platform-native innovation, or to constrain where code goes. Those prove to be limitations, as platforms further evolve and as your feature set expands. The strategy for cross-platform apps also applies to cross-platform cloud. Trying to abstract yourself away from a cloud platform will further complicate your cloud strategy, not simplify it. The proof points and experience are exactly the same as on the client.

Massive security breaches challenge the enterprise platform.

2014 will go down as the “year of the massive security breach.” Target, eBay, J.P. Morgan, Home Depot, Nieman Marcus, P.F. Chang’s, Michaels, Goodwill and, finally, Sony were just some of the major breaches this year. This next year will be defined by how enterprises respond to the breach.

First, the biggest risks are endpoints. Endpoints as defined by today’s technology are likely vulnerable in just about all circumstances, and show no signs of abating. Second, the on-prem data-center infrastructure suffers this same limitation. Together, the two make for a very challenging situation. The reason is not because today’s infrastructure is poorly designed or managed, but because of the combination of an architecture designed for another era and a sophistication level of nation-state opponents that exceeds IT’s ability to detect, isolate and remediate. As fatalistic as it sounds, this is a new world. Former DHS Secretary Tom Ridge said in an interview, “[T]here are two types of companies: Those that know they have been hacked by a foreign government and those that have been hacked and don’t know it yet.”

The challenge for 2015 in this year of adapting to new technologies is managing through the change. The good news is that there are tools and approaches that can make a huge difference. This post picked many trends that taken together are about this theme of securing a modern enterprise. If you use public cloud services on next-generation platforms you aren’t guaranteed security, but it is highly likely that the team has assembled more talent and has an existential focus on security that is very difficult for most enterprises to duplicate. If you use cloud services rather than local or LAN storage for documents, not only do you gain many features, but you gain a level of security you otherwise lack. Not only is this counterintuitive, it is challenging to internalize on many dimensions. It is also the only line of sight to a solution.

As endpoints, the combination of a modern mobile OS and apps is a new level of security and quality. The most innovative and forward-looking solutions in security will be found in startups taking new approaches to these challenges. Even looking at basics, deploying enterprise-wide single-sign-on with mobile-phone-based two-factor would be a substantial and immediate win that accrues to both legacy solutions and cloud solutions.

Technologies to watch in 2015

Above represents some challenges in the extreme, but also a huge opportunity to cross the chasm into a mobile and cloud-centric company or enterprise. Even with all that is going on to get that work done, this will also be a year where some new technologies will make their appearance or begin to wind their way through early adopters. The following are just some technologies I will be watching for (particularly at the Consumer Electronics Show in January):

Beacon. To some, beacon is still a solution searching for a problem, but I think we are on the cusp of some incredibly innovative solutions. I have been playing with beacons and encourage startups that have any potential to use location to do the same. In terms of enterprise productivity, beacons plus a conference room or auditorium is one area where some incredibly innovative tools can be developed.

4K and beyond. Moore’s law applied to pixels has been incredible. Apple’s 5K iMac topped off a year where we saw 4K displays for hundreds of dollars. In mobile, pixel density will increase (to the degree that battery life, OS and hardware can keep up) and for desktop and wall, screen size will continue to increase. Wall-sized displays, wireless transmission and hopefully touch will introduce a whole new range of potential solutions for collaboration, signage and education.

Tablet keyboards. I am definitely biased in this regard, but I am looking forward to seeing a strong combination of tablets, keyboards and mobile OS enhancements. If you’re developing tablet apps, I’d make sure you’re testing them out with keyboards, as well. The idea that a laptop clamshell form factor can be a mobile OS is going to be normal by the end of the year. The need to convert between “tablet mode” and “laptop mode” isn’t a critical feature for productivity, especially for large screen size. Physical keys will define a clamshell, and make converting to a “tablet” awkward. Innovative touch-based covers could make a resurgence for smaller tablet form factors.

The following is a set of “everyday” things you can do, starting immediately. They are easy. They almost certainly require a behavior change. They will make a difference.

Payments. Apple Pay arrived in 2014 and will have a huge impact on how we view payments. Yet the feature set and usage are still maturing. The transformation of payments will take a long time but happen much faster than many think or hope. I am optimistic about traditional bank accounts, credit cards, currencies all being transformed by the block chain and mobile. Because of the immense infrastructure in the developed world, it is likely the developing world will be leaders in payment and banking.

APIs. One of the most interesting differentiators of cloud services is the way APIs are offered and consumed. Every cloud service offers APIs that are easily consumed at the right abstraction levels. In the old days, a client-server API would look like SQL tables. Today, this same API works the way you think about developing custom apps, time to solution is greatly reduced, and integration with other services is straightforward. I’ll be on the lookout for services with cool APIs and services that take advantage of APIs used by other services.

Machine-learning services. Artificial intelligence has always been five years away. I can safely say that has been the case at least for my entire programming lifetime, starting with, “Would you like to play a game?” Things have changed dramatically over the past year. We now see ML as a service, even from IBM. The ability to easily get to large corpora and to efficiently compute training data in cloud-scale servers is a gift. While it is likely that everything will be marketed using ML terms, the real win will be for those building products to just use the services and deliver customer benefit from them. I’m keeping an eye on opportunities for machine learning to improve products.

On-demand. On-demand is redefining our economy. In many places, a few people still view on-demand as a “spoiled San Francisco” thing. As you think about it, on-demand and same-day delivery bring a new level of efficiency, reduction in traffic, pollution, congestion, infrastructure and more. It is one of those things that is totally counterintuitive until you experience it, and until you start to think about the true costs of consumer-facing storefronts and supply chain. On-demand will be viewed as a macro-efficient necessity, not a super-luxury convenience.

From the coffee shop to the boardroom, 2015 will be a year of big leaps for everyone, as we tap into the new normal and execute on a foundation of new services, new paradigms and new platforms.

Going Where the Money Isn’t: Wi-Fi for South African Townships

Spending time in Africa, one is always awestruck. The continent has so much to offer, from sands to rain forests, from apes to zebras, from Afrikaans to Zulu. More than 1.1 billion people, 53 countries and at least 2,000 different spoken languages make for amazing diversity and energy.

Spending time in Africa, one is always awestruck. The continent has so much to offer, from sands to rain forests, from apes to zebras, from Afrikaans to Zulu. More than 1.1 billion people, 53 countries and at least 2,000 different spoken languages make for amazing diversity and energy.

Yet even while spending just a little time, you quickly see the economic challenges faced by many — slums, townships, settlements and the poverty they represent are seen too frequently. The contrast with the developing world is immense. As a visitor, you’re not particularly surprised to find the difficulties in staying connected to wireless services that you’ve become reliant upon.

We hear about the mobile revolution in Africa all the time. Today, this is a revolution in voice and text on feature phones and increasingly on smartphones, phablets and small tablets. Smartphones are making a rapid rise in use, if for no other reason than they have become inexpensive and ubiquitous on the world stage, and also thanks, in part, to reselling of used phones from developed markets.

But keeping smartphones connected to the Internet is straining the spectrum in most countries, and is certainly straining the connectivity infrastructure. Africa, for the most part, will “skip over” PCs, as hundreds of millions of people connect to the Internet exclusively by phones and tablets. But there’s an acute need for improved connectivity.

The problem is that, even in the most developed areas of Africa, the deployment of strong and fast 3G and 4G coverage is lagging, and the capital that is available will flow to build out areas where there are paying customers. That means that the outlying areas, where a lot of people live, will continue to be underserved for quite some time.

Alan Knott-Craig, an experienced South African entrepreneur who is setting out to bring connectivity via Wi-Fi across his homeland, knows that Internet access is transformative to those in slums and townships. His previous company, Mxit, where he was CEO, developed a wildly popular social network for feature phones. It delivered a vast array of services, from education to community to commerce, and is in use by tens of millions.

Given the challenges of connectivity in Africa, you often find yourself searching for a Wi-Fi connection for any substantial browsing or app usage. The best case — except for a couple of markets and capital cities — is that you will get a strong 3G and occasional 4G that is highly dependent on carrier and location. It is not uncommon for folks to have smartphones that are used for voice and text when on the network, and apps that are used only when there is Wi-Fi. It’s not just a way to save money or avoid your data cap — Wi-Fi is a necessity.

“Going where the money isn’t”

One can imagine there’s a big business to be had building out the Wi-Fi hotspot infrastructure in the country. Knott-Craig recognized this as he began to explore how to bring connectivity to more people.

Having grown up in South Africa and deeply committed to both the social and business needs of the country, Knott-Craig has also dedicated his businesses to those who are least well served and would benefit the most. Over the past 20 years, the improvements in service delivery to the slums and townships of South Africa have improved immensely, reducing what once seemed like an insurmountable gap. While there is clearly a long way to go, progress is being made.

The transformation that mobile is bringing to townships is almost beyond words to those who are deeply familiar with the challenges. Talking and texting with family and friends are great and valuable. A mobile phone brings empowerment and identity (a phone number is the most reliable form of identity for many) in ways that no other service has been able to. Access to information, education and community all come from mobile phones. Mobile is a massive accelerator when it comes to closing economic divides.

All too often in business, the path is to build a business around where the money is. Knott-Craig’s deep experience in mobile communications told him that the major carriers will address connectivity in the cities and where there is already money. So, in his words, he set out to improve mobile connectivity by “going where the money isn’t.”

It was obvious to Alan that setting up Wi-Fi access would be transformative. The question was really how to go about it.

Building bridges

Time and again, one lesson from philanthropy is that the solutions that work and endure are the ones that enroll the local community. Services that are created by partnerships between the residents of townships, the government and business are the only way to build sustainable programs. The implication is that rolling into town with a bunch of access points and Internet access sounds like a good idea — who wouldn’t want connectivity? — but in practice would be met with resistance from all sides.

Thinking about the parties involved, Knott-Craig created Project Isizwe — helping to deliver Wi-Fi to townships on behalf of municipalities. “Isizwe” is Xhosa for “nation,” “tribe” or “people.”

In the townships, people pay for Internet access by the minute, by the text and by the megabyte. Rolling out Wi-Fi needed to fit within this model, and not create yet another service to buy. So the first hurdle to address would be to find a way to piggyback on that existing payment infrastructure.

To do this, Knott-Craig worked with carriers in a very smart way. Carriers want their customers on the Internet, and in fact would love to offload customers to Wi-Fi when available. While they can do this in densely populated urban areas where access points can be set up, townships pose a very different environmental challenge, discussed below.

Given the carriers’ openness to offloading customers to Wi-Fi, the project devised a solution based on the latest IEEE standards for automatically signing on to available hotspots (something that we wish we would experience in practice in the U.S.). A customer of one of the major carriers, MTN for example, would initiate a connection to the Isizwe network, and from then on would automatically authenticate and connect using the mobile number and prepaid megabytes, just as though the Wi-Fi were a WWAN connection.

This “Hotspot 2.0″ implementation is amazingly friendly and easy to use. It removes the huge barrier to using Wi-Fi that most experience (the dreaded sign-on page), and that in turn makes the carriers very happy. Because of the value to the carriers, Knott-Craig is working to establish this same billing relationship across carriers, so this works no matter who provides your service.

Of course this doesn’t solve the problem of where the bandwidth comes from in the first place. Since Knott-Craig is all about building bridges and enrolling support across the community, he created unique opportunities for those that already have unused bandwidth to be part of the solution.

Whether it is large corporations or the carriers themselves, Project Isizwe created a wholesale pool of bandwidth by either purchasing outright or using donated bandwidth to create capacity. The donated bandwidth provides a tax deduction benefit at the same time. Everyone wins. Interestingly, the donated bandwidth makes use of off-peak capacity, which is exactly when people in the townships want to spend time on the Internet anyway.

Government

With demand and supply established, the next step is to enroll the government. Here again, the team’s experience in working with local officials comes into play.

As with any market around the world, you can’t just put up public-use infrastructure on public land and start to use it. The same thing is true in the townships of South Africa. In fact, one could imagine an outright rejection of providing this sort of service from a private organization, simply because it competes with the service delivery the government provides.

In addition, the cost factor is always an issue. Too many programs for townships start out free, but end up costing the government money (money they don’t have) over time. It isn’t enough to provide the capital equipment and ask the government to provide operational costs, or vice versa. Project Isizwe is set up to ensure that public free Wi-Fi networks are a sustainable model, but needed government support to do so.

With the enrollment of the carriers and community support, bringing along the government required catering to their needs, as well. One of the biggest challenges in the townships is the rough-and-tumble politics — not unlike local politics in American cities. The challenge that elected officials have is getting their voice heard. Without regular television coverage, and with sporadic or limited print coverage, the Internet has the potential to be a way for the government to reach citizens.

As part of the offering, Knott-Craig and his team devised a platform for elected officials to air their point of view through “over the top” means. Essentially, part of the Wi-Fi service provides access to a public-service “station” filled with information directly from governmental service providers. Because of the nature of the technology, these streams can be cached and provided at an ultra-low cost.

The bottom line for government is that they are in the business of providing basic services for the community. Providing Internet access only adds to the menu of services, including water, electrical, sanitation, police, fire and more. Doing so without a massive new public program of infrastructure is a huge part of what Isizwe did to win over those officials.

Access points

With all the parties enrolled, there still needs to be some technology. It should come as no surprise that setting up access points in townships poses some unique challenges: Physical security, long-haul connectivity and power need to be solved.

One of the neat things about the tech startup ecosystem in South Africa is the ability to draw on resources unique to the country. The buildup of military and security technology, particularly in Pretoria, created an ecosystem of companies and talent well-suited to the task. Given the decline of these industries, it turns out that these resources are now readily available to support new private-sector work.

First up was building out the access points themselves. Unlike a coffee shop, where you would just connect an access point to a cable modem and hide it above a ceiling tile, townships have other challenges. Most of the access points are located high up in secured infrastructure, such as water towers. These locations also have reliable power and are already monitored for security.

The access points are secured in custom-designed enclosures, and use networking equipment sourced from Silicon Valley companies Ruckus Wireless and Ubiquiti Networks, which implement hotspots around the world. This enclosure design and build was done by experienced steel-manufacturing plants in Pretoria. In addition, these enclosures provide two-way security cameras with night vision to monitor things.

This provided for a fun moment the first time someone signed on. A resident had been waiting for the Wi-Fi and was hanging out right below the tower. As soon as they signed on for the first time, back at the operations center they could see this on the dashboard, as well as the camera, and used the two-way loudspeaker to ask, “So how do you like the Wi-Fi?” which was quite a surprise to a guy just checking football scores on his mobile phone.

Along with using engineers from Pretoria to design the enclosure, Isizwe also employed former military engineers to go on-site to install the access points. This work involved two high-risk activities. First, these men needed to climb up some pretty tall structures and install something not previously catered for. Their skills as linemen and soldiers helped here.

More importantly, these were mostly Afrikaner white men venturing into the heart of black townships to do this work. Even though South Africa is years into an integrated and equality-based society, the old emotions are still there, just as has been seen in many other societies.

This would be potentially emotionally charged for these Afrikaners in particular. No only were there no incidents, but the technicians were welcomed with open arms, given the work that they were doing — “We are here to bring you Wi-Fi” — turns out to make it easy to put aside any (wrongly) preconceived notions. In fact, after the job, the installers were quite emotional about how life-changing the experience was for them to go into the townships for the first time and to do good work there.

The absence of underground cabling presents the challenge of getting these access points on the Internet in the first place. To accomplish this, each access point uses a microwave relay to connect back up to a central location, which is then connected over a landline. This is a huge advantage over most Wi-Fi on the African continent, which is generally a high-gain 3G WWAN connection that gets shared over local Wi-Fi.

Bytes flowing

The service is up and running today as a 1.0 version, in which Wi-Fi is free but limited to 250 megabytes; the billing infrastructure is just a few months away, which will enable pay-as-you-go usage of megabytes. The service will be free when there is capacity going unused.

The cost efficacy of the system is incredible, and that is passed along to individual users. Wi-Fi is provided at about 15 cents (ZAR cents) per gigabyte, which compares to more than 80 cents per megabyte for spotty 3G. That is highly affordable for the target customers.

Because of the limits of physics of Wi-Fi, the system is not set up to allow mass streaming of football, which is in high demand. Mechanisms are in place to create what amounts to over-the-top broadcast by using fixed locations within the community.

The most popular services being accessed are short videos on YouTube, music, news, employment information and educational services like Khan Academy and Wikipedia. The generation growing up in the townships is even more committed to education, so it is no surprise to see such a focus. Another important set of services being accessed are those for faith and religion, particularly Christian gospel content.

The numbers are incredible and growing rapidly, as the Isizwe scales to even more townships. In the middle of the afternoon (when people are at school and working), we pulled up the dashboard and saw some stats:

- 609 people were online right at that moment.

- 4,455 people had already used the service that day.

- 304 people had already reached their daily limit that day.

- More than 70,000 unique users since the system went online with 1.0 in November 2013.

- 208GB transferred since going online

- Most all of the mobile traffic is Android, along with the newest Asha phones from Nokia. Recycled iPhones from the developed market also make a showing.

In terms of physical infrastructure required, it takes about 200 access points to cover a densely populated area of one million residents. This allows about 200,000 simultaneous users overall, with about 50-500 users per access point, depending on usage and congestion.

Growing

We talk all the time about the transformational nature of mobile connectivity, and many in the U.S. are deeply committed to getting people connected all around the world. Project Isizwe is an incredible example of the local innovation required to build products and services to deliver on those desires.

The public/private/community partnerships that are the hallmark of Isizwe will scale to many townships across South Africa. Building on this base, there are many exciting information-based services that can be provided. Things are just getting started.

–Steven Sinofsky (@stevesi)

This post originally appeared on Re/code.

Disrupting Payments, Africa Style

Note from the author: For the past 10 years or so, I’ve been spending time informally in Africa, where I have a chance to visit with government officials, non-government organizations, and residents of towns, settlements and cities. In the next post, I’ll talk about free Wi-Fi in South Africa slums. This post originally appeared on Re/code.

Spending time in the developing world, one can always marvel at the resourcefulness of people living in often extraordinarily difficult conditions. The challenges of living in many parts of the world certainly cause one to reflect on what we see from day to day. Here in the U.S., we’re all familiar with the transformative nature of mobile phones in our lives. And for those in extreme poverty, the mobile phone has been equally, if not more, transformative.

One particular challenge faced by many in Africa, especially those living in fairly extreme poverty (less than $500 a year in purchase power), is dealing with money and buying things, and how the mobile phone is transforming those needs.

One could fill many posts with what it is like to live at such low levels of income, but suffice it to say that even when you are fortunate enough to ground your perspective in firsthand experience, it is still not possible to really internalize the challenges.

Slum life

Imagine living in a place where your small structure, like the one pictured below, is under constant threat of being demolished, and you run the risk of being relocated even farther away from work and family. Imagine a place where you don’t have the means of contacting the police, even if they might show up. Imagine a place where it takes a brick-sized amount of cash to buy a new cooking pot.  Representative home, or “struct,” in an informal settlement in the suburbs of Harare, Zimbabwe. Steven Sinofsky

Representative home, or “struct,” in an informal settlement in the suburbs of Harare, Zimbabwe. Steven Sinofsky

These and untold more challenges define day-to-day life in slums, settlements and townships in developing countries in Africa, where the introduction of mobile phones has transformed a vast array of daily living tasks. Take the structure seen above, for example. It is a settlement in a vacant lot next to an office park in Harare, Zimbabwe. About 120 of these “structs” are occupied by about 600 people. For the most part, residents sell what they can make or cook; a small number possess some set of trade skills. Below, you can see a stand run out of one struct that sells eggs farmed on-site.

Shop window in front of home where fresh eggs are sold in an informal settlement in the suburbs of Harare, Zimbabwe. Steven Sinofsky.

Shop window in front of home where fresh eggs are sold in an informal settlement in the suburbs of Harare, Zimbabwe. Steven Sinofsky.

Mobile phones and extreme poverty

Through a Xhona-speaking interpreter, I had a chance to be part of a group (representing the government) hearing about life in the settlement. One question I got to ask was how many had mobile phones. Keeping in mind that the per capita spending power of these folks would be formally labeled “extreme poverty,” the answer blew me away. Nearly every adult had a mobile phone. When I asked for a show of hands, some proudly said they didn’t bring it to the meeting.

Group of representatives showing off their mobile phones (all pictured owned a phone) of an informal settlement in the suburbs of Harare, Zimbabwe. Steven Sinofsky

Group of representatives showing off their mobile phones (all pictured owned a phone) of an informal settlement in the suburbs of Harare, Zimbabwe. Steven Sinofsky

Right away, you see the importance of a mobile phone when you consider the cost of the phone as a percentage of income. It is hard for us to imagine the trade-offs phone owners here are making, but in earning-power equivalence, a phone in this village is roughly what a car and its operation costs us — and we already have food, shelter and clothing in ample supply.

Communicating with family is a key function, because families are often separated by distance, as members go looking for work or to find a better place to live.

Phones are also used to call the police. Before mobile phones, there was simply no way to get the police to your home or settlement, since there are no landlines or nearby telephones. Keep in mind that most residents in these areas have no formal identification or address, and the settlements are often unofficial and unrecognized by authorities.

Phones are also used as an early warning system for authorities that might be on the way to evict folks, or perhaps perform some other type of inspection. The legalities of settlements and how that works are a separate topic altogether, but I won’t go into that here.

Phones are used to keep track of what goods are selling where, or what goods might be needed. A network of people helps each other to maximize income from goods based on where and when they can be sold, because they are needed. Think of this as extremely local information that was previously unavailable. This is crucial, because many goods have limited shelf life and, frankly, many people produce the same goods.

A specific example for some people was the use of phones to monitor the supply chain for beer and alcohol. One set of people specialized in redistribution of beverages, and needed to keep tabs on events and unique needs in the community.

A favorite example of mine is “queue efficiency.” One of the many challenging aspects of life in extreme poverty is waiting — waiting on line for water, for transportation, for public services of all kinds. Phones play an important role in bringing some level of optimization to this process by sharing information on the size of queues and the quality of service available. We might think of this as Waze for lines, implemented over SMS friends and family networks.

Some of these uses seem straightforward, or simply cultural adaptations of what anyone with a phone would do. The fact that Africa skipped landlines is a fascinating statement about technological evolution — just as, for the most part, the continent will skip PCs in favor of smartphones, and will likely skip private ownership of transportation for shared-economy solutions (the history of Lyft is one that begins with shared rides in Zimbabwe).

Skipping over traditional banking

An old-economy service that Africa is likely to skip will be personal banking. In the U.S., our tech focus tends to be on China and the role that mobile payments play there with WeChat or AliPay, or more broadly on the innovation going on payments between the innovative PayPal, Square and, of course, bitcoin. In Africa, almost no one has a bank account, and definitely no credit cards. But as we saw, everyone has a mobile phone.

The most famous mobile banking solution in Africa is M-Pesa (M for mobile, pesa is Swahili for money), which started in Kenya. People there use their phones to store cash and pay for goods. Similar solutions exist in many countries. Even in a place as remote and difficult as Somaliland, you can see these at work, as I did recently.

Madagascar is an island-country with incredible beauty and an abundance of things not seen across Africa, including natural resources, farmable land and water, not to mention lemurs. Yet the country is incredibly poor, with a countrywide per capita GDP of $400, which puts it in the bottom 10 countries of the world. On average, people live at the extreme poverty level of $1.25 per day in purchase power. One city I visited in Madagascar is home to the UN Millennium Development Goals, which is programmatically working to improve these extremely impoverished areas.

Sign signifying the entrance to a town in rural Madagascar designated a Millennium Development Goals location, one of about a dozen worldwide. Steven Sinofsky

Sign signifying the entrance to a town in rural Madagascar designated a Millennium Development Goals location, one of about a dozen worldwide. Steven Sinofsky

Yet technology is making a huge difference in lives there. Madagascar has three main mobile phone carriers. These are all prepay, and penetration is extremely high, even in the most remote areas. The country is wired with mostly 2G connectivity; there is some coverage at 3G, but it is highly variable. The only common use for 3G is for Internet access using external USB modems connected to PCs (usually netbooks) and shared.

Most of the phones in use are feature phones, often hand-me-downs from the developed market. I’ve even seen a few iPhone 3s. One person complained about being unable to update iOS because he has no high-speed connection for such a download (showing that people are connected to the world, just not at a high download speed). A developed-market smartphone is pretty much a feature phone here, and the cost of another network upgrade means that one is far off. People are anxious for more connectivity, but along with cost, the current state of government will make progress a bit slower than citizens would like.

A huge problem in this type of environment is safely dealing with money. Madagascar’s currency trades at $1 U.S. to 2,500 Madagascar ariary. When you live off of 3,000 or so a day, you’re not going to carry around three bills, so very quickly you end up with a brick of 100 Ar notes. What to do with all those? Where can you put them? How do you keep them safe? How can you even keep them dry in a rain forest?

Well, along comes mobile “banking.” As easy as you can recharge your phone, you can add money to your stored money account. You walk up to a kiosk — there are thousands and thousands of them — and in a series of text messages with the shopkeeper, you give her money and your phone gains stored value.

Home and storefront selling recharge minutes for pay-per-use mobile phones; also a station for mobile-phone banking in rural Madagascar. Steven Sinofsky

Home and storefront selling recharge minutes for pay-per-use mobile phones; also a station for mobile-phone banking in rural Madagascar. Steven Sinofsky

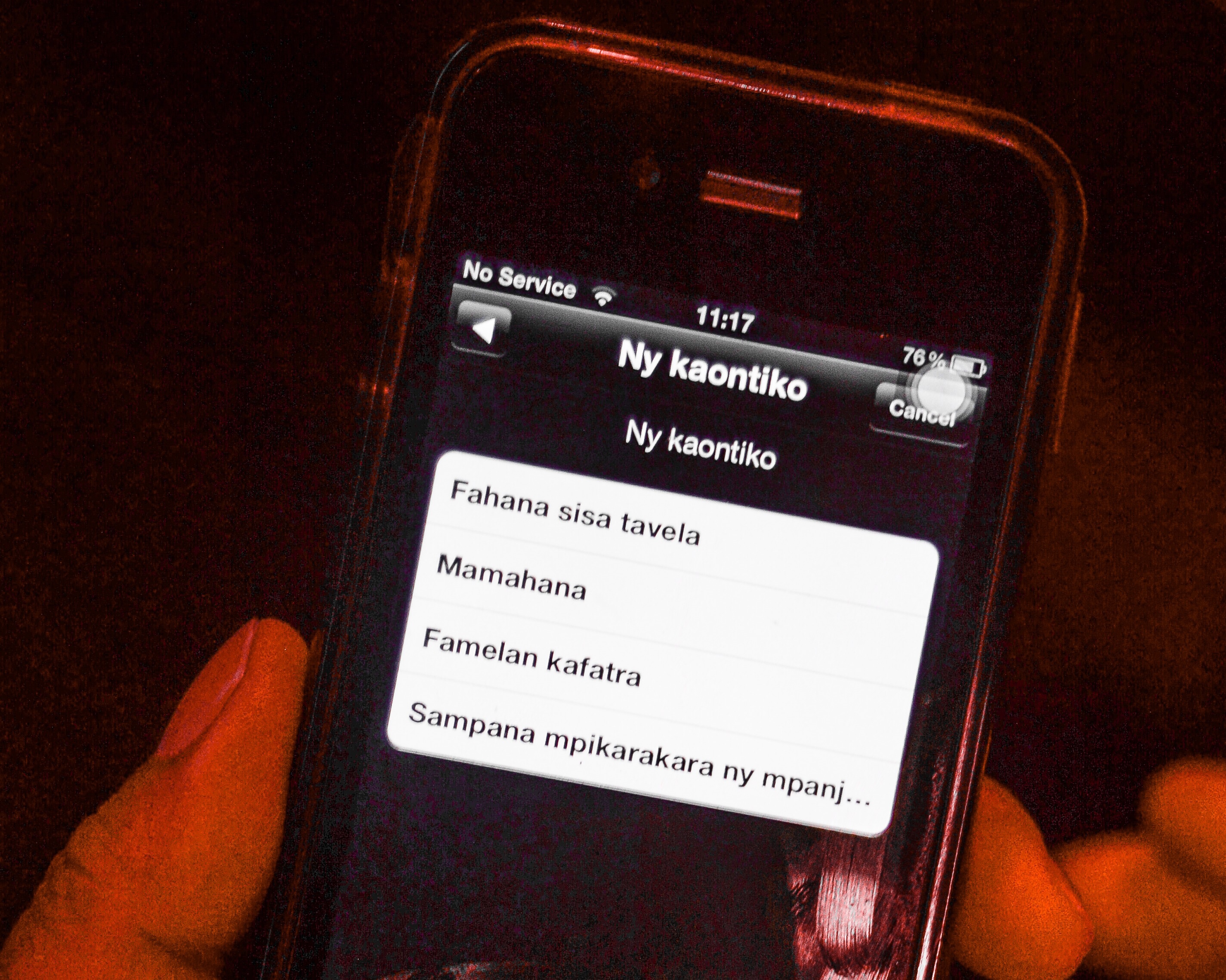

With iOS and Android fragmentation, how would these apps work, given what must be finite dev resources? The implementation of this is all through an old-school standard called SIM Apps or Sim Application Toolkit.

This set of APIs and capability allow the installation of apps that reside on your SIM. These apps are simple menu-driven apps that look like WAP sites. They are secure and controlled by carriers. Using this framework, mobile banking has reached unprecedented usage and importance in developing markets, particularly in Africa.

The scenario for usage is quite simple. You charge your phone with money, just as you would with minutes. When you want to buy something, you bring up the SMS app (pictured below, on an iPhone 3 in Malagasy) and initiate a transaction. The merchant gives you a code, which you enter along with the merchant’s identifying code. You then type in an amount, which is verified against your current balance. The merchant then receives a notification, and the transaction is complete. The whole system is safe from theft because of the connection to your mobile number, two-factor authentication and so on. There is no carrier dependency, so you can easily send/receive to any carrier, though the carrier has your balance. This isn’t an interest-earning savings account, but rather a transaction or debit account (of course, in the U.S., few of us earn interest on demand deposits these days, anyway).  Screen showing “My Account” in Malagasy, displayed on a recycled iPhone 3 (note the absence of a cellular connection). Steven Sinofsky

Screen showing “My Account” in Malagasy, displayed on a recycled iPhone 3 (note the absence of a cellular connection). Steven Sinofsky

You can also give and receive money from individuals. This is extraordinarily important, given how there can be distance between family or even the main wage-earning in a family. The idea of sending money around to family members is an incredibly important part of the cash economy of low-income people. This market, called “remittance,” is estimated to be over $400 billion in developing markets alone.

Life is easier and safer for those using mobile banking this way. You can count on your money being safe. You don’t need to carry around cash and worry about loss, theft, or water and weather destroying physical currency. You can easily deal with small and exact amounts. As a merchant, you don’t have to make change. It is just better in every dimension.

The carriers profit by taking a percentage of the transaction, which is high in the same way that check-cashing in the U.S. is high (and credit cards, for that matter). The fee is about two percent, which I am not sure will be sustainable, given the competition between carriers. I also think it will be fascinating to see how developed-market companies like Western Union evolve to support mobile payments, as they provide integration points to the developed-market financial systems. It is not uncommon to see a Western Union representative also offering phone recharge and mobile banking services.

In our environment, we would see this as a convenience, like a debit card. But in Africa, it is far more secure and convenient, because you only need your phone, which you will carry with you almost all the time, just as we do in the U.S.

I think the most interesting point of note in this solution is how it essentially skips over banking. If we think about our own lives, and especially those of the generation entering the workforce now, banking is most decidedly archaic. The whole idea of opening an account and dealing with a level of indirection which offers very little by way of useful services — it just feels like there’s a need for disruption. Our installed base of infrastructure makes this very difficult, but in the developing world that challenge doesn’t exist. It isn’t likely that most people will graduate to full-fledged banking just as we don’t expect people to graduate from a mobile phone to a full-fledged PC.

It also isn’t hard to imagine this type of mobile banking taking off first in the cash-based part of the developed world, where today people pay fees to cash checks and buy money orders, absent a bank account. The large numbers of check-cashing storefronts located near lower-income areas share much in common in some ways. One example is remittance. Many immigrants in the U.S. are the source for remittance funds going to developing markets. Seattle, for example, has one of the largest populations of Somalians outside of Northern Africa, and they routinely send funds back to their families. Today, this is a difficult process, and could be made a lot easier with a global and mobile solution.

Looking forward

Merchant using a credit-card reader attempting to get a stronger signal to complete the transaction in Anosibe, Madagascar. Steven Sinofsky

I look forward to solutions like this for our own lives here in the U.S. We see some of this in service-by-service cases. For example, using Lyft is completely cashless. I can use PayPal at merchants like Home Depot. Obviously, we all see Square and other payment mechanisms. Each of these shares a common connection to established banking and plastic cards. That’s where I think disruption awaits. Will this be bitcoin alone? Will someone, even a carrier, develop and scale a simple stored-value mechanism like that being used by billions of people already?

For myself, and no doubt for many reading this, this transformation is old hat. I’ve seen these changes over the past decade across many countries in Africa and elsewhere. Africa isn’t single-marketplace by any stretch. What is working in Madagascar, Kenya, Somaliland and others might not work elsewhere, or might not work for all segments of a given economy. Stay tuned for more observations from this trip.

It is always worth a reminder how some changes can bring about a massive difference in quality of life.

–Steven Sinofsky @stevesi

P.S.: What happens when you’re forced to use high-tech 3G connectivity to do a Visa card transaction? The merchant (pictured above) goes outside in a rain forest and aims for a stronger connection for the card reader. Yikes!

#codecon and reflecting on generational changes

Attending the <code/conference> (#codecon) this past week turned out to be a remarkable experience, even more remarkable than I expected. The generational shift in our computing experience from desktop to mobile, from software to services, and from hundreds of millions to trillions was on display through the interviews with a dozen industry CEOs.

Attending the <code/conference> (#codecon) this past week turned out to be a remarkable experience, even more remarkable than I expected. The generational shift in our computing experience from desktop to mobile, from software to services, and from hundreds of millions to trillions was on display through the interviews with a dozen industry CEOs.

This post will explore this generational change through the speakers at the conference. Before diving into the details of each session, we will explore this change and the implicit context.

Generational Change

Reflecting on the interviews and demonstrations as well as the “lobby chatter” is a key part of learning by attending. I’ve always viewed this conference and predecessor D Conference as the most relevant conferences for learning about the strategic drivers of our industry. You can read my report from last year here. Writing these reports is part of the learning for me and reading the old reports lets me checkpoint on my own learning and journey.

If you move beyond the insights from any single speaker or the announcements at the event (all were widely reported by re/code and others and new this year by re/code partner CNBC), one theme just keeps coming back to me—the vast difference in tone and content between the incumbents and the challengers, between legacy and disruptors, between the old guard and the new, or whatever labels you want to use. We talk all the time about the transition of our industry from one era to another (and don’t forget the term “post-PC” was first used in this very forum) and the conference provides a microcosm expressed through leaders of these transitions taking place.

There is a vast difference in tone and content between the incumbents and the challengers, between legacy and disruptors, between the old guard and the new.

The transition is in full force. This does not mean by definition that all existing companies will lose and only new companies will win. Quite the contrary, the fact that these changes are now visible to all makes the creation, purchase, and use of new products and technologies evidence of the transition, as well as opportunity to create new plans and adjust. The mobile internet is causing the transition but also making the communication of that very transition much more transparent, which is unlike the progressive unveiling that characterized the mainframe to mini to PC transition.

Are the new companies doing enough to transition customers as well as their own business to new paradigms? How much should new companies bridge from existing solutions or should they expect a wholesale change from customers? Is there an understanding of the existing complexities of the real world?

Are the incumbents changing enough to build new products and business that reflect the new generation? Are they trying too much to “thread the needle” and incrementally step to a new context by maintaining status quo or “repotting the plants”? Is there an understanding of the complexities of existing solutions?

The puts this "generational" change out there for us to experience through the always challenging, yet always consistently even-handed questioning (interrogation) from Walt and Kara (and a great addition this year were interviews featuring seasoned members of the re/code team).

Context (is everything in business)

The attendees (in the audience) are people who have worked in the industry often times since the earliest days. The interviewers are professionals who cover deeply the industry and the subjects. It is hard to imagine creating a more informed or tougher environment. That’s the challenge.