Archive for July 2014

Disrupting Payments, Africa Style

Note from the author: For the past 10 years or so, I’ve been spending time informally in Africa, where I have a chance to visit with government officials, non-government organizations, and residents of towns, settlements and cities. In the next post, I’ll talk about free Wi-Fi in South Africa slums. This post originally appeared on Re/code.

Spending time in the developing world, one can always marvel at the resourcefulness of people living in often extraordinarily difficult conditions. The challenges of living in many parts of the world certainly cause one to reflect on what we see from day to day. Here in the U.S., we’re all familiar with the transformative nature of mobile phones in our lives. And for those in extreme poverty, the mobile phone has been equally, if not more, transformative.

One particular challenge faced by many in Africa, especially those living in fairly extreme poverty (less than $500 a year in purchase power), is dealing with money and buying things, and how the mobile phone is transforming those needs.

One could fill many posts with what it is like to live at such low levels of income, but suffice it to say that even when you are fortunate enough to ground your perspective in firsthand experience, it is still not possible to really internalize the challenges.

Slum life

Imagine living in a place where your small structure, like the one pictured below, is under constant threat of being demolished, and you run the risk of being relocated even farther away from work and family. Imagine a place where you don’t have the means of contacting the police, even if they might show up. Imagine a place where it takes a brick-sized amount of cash to buy a new cooking pot.  Representative home, or “struct,” in an informal settlement in the suburbs of Harare, Zimbabwe. Steven Sinofsky

Representative home, or “struct,” in an informal settlement in the suburbs of Harare, Zimbabwe. Steven Sinofsky

These and untold more challenges define day-to-day life in slums, settlements and townships in developing countries in Africa, where the introduction of mobile phones has transformed a vast array of daily living tasks. Take the structure seen above, for example. It is a settlement in a vacant lot next to an office park in Harare, Zimbabwe. About 120 of these “structs” are occupied by about 600 people. For the most part, residents sell what they can make or cook; a small number possess some set of trade skills. Below, you can see a stand run out of one struct that sells eggs farmed on-site.

Shop window in front of home where fresh eggs are sold in an informal settlement in the suburbs of Harare, Zimbabwe. Steven Sinofsky.

Shop window in front of home where fresh eggs are sold in an informal settlement in the suburbs of Harare, Zimbabwe. Steven Sinofsky.

Mobile phones and extreme poverty

Through a Xhona-speaking interpreter, I had a chance to be part of a group (representing the government) hearing about life in the settlement. One question I got to ask was how many had mobile phones. Keeping in mind that the per capita spending power of these folks would be formally labeled “extreme poverty,” the answer blew me away. Nearly every adult had a mobile phone. When I asked for a show of hands, some proudly said they didn’t bring it to the meeting.

Group of representatives showing off their mobile phones (all pictured owned a phone) of an informal settlement in the suburbs of Harare, Zimbabwe. Steven Sinofsky

Group of representatives showing off their mobile phones (all pictured owned a phone) of an informal settlement in the suburbs of Harare, Zimbabwe. Steven Sinofsky

Right away, you see the importance of a mobile phone when you consider the cost of the phone as a percentage of income. It is hard for us to imagine the trade-offs phone owners here are making, but in earning-power equivalence, a phone in this village is roughly what a car and its operation costs us — and we already have food, shelter and clothing in ample supply.

Communicating with family is a key function, because families are often separated by distance, as members go looking for work or to find a better place to live.

Phones are also used to call the police. Before mobile phones, there was simply no way to get the police to your home or settlement, since there are no landlines or nearby telephones. Keep in mind that most residents in these areas have no formal identification or address, and the settlements are often unofficial and unrecognized by authorities.

Phones are also used as an early warning system for authorities that might be on the way to evict folks, or perhaps perform some other type of inspection. The legalities of settlements and how that works are a separate topic altogether, but I won’t go into that here.

Phones are used to keep track of what goods are selling where, or what goods might be needed. A network of people helps each other to maximize income from goods based on where and when they can be sold, because they are needed. Think of this as extremely local information that was previously unavailable. This is crucial, because many goods have limited shelf life and, frankly, many people produce the same goods.

A specific example for some people was the use of phones to monitor the supply chain for beer and alcohol. One set of people specialized in redistribution of beverages, and needed to keep tabs on events and unique needs in the community.

A favorite example of mine is “queue efficiency.” One of the many challenging aspects of life in extreme poverty is waiting — waiting on line for water, for transportation, for public services of all kinds. Phones play an important role in bringing some level of optimization to this process by sharing information on the size of queues and the quality of service available. We might think of this as Waze for lines, implemented over SMS friends and family networks.

Some of these uses seem straightforward, or simply cultural adaptations of what anyone with a phone would do. The fact that Africa skipped landlines is a fascinating statement about technological evolution — just as, for the most part, the continent will skip PCs in favor of smartphones, and will likely skip private ownership of transportation for shared-economy solutions (the history of Lyft is one that begins with shared rides in Zimbabwe).

Skipping over traditional banking

An old-economy service that Africa is likely to skip will be personal banking. In the U.S., our tech focus tends to be on China and the role that mobile payments play there with WeChat or AliPay, or more broadly on the innovation going on payments between the innovative PayPal, Square and, of course, bitcoin. In Africa, almost no one has a bank account, and definitely no credit cards. But as we saw, everyone has a mobile phone.

The most famous mobile banking solution in Africa is M-Pesa (M for mobile, pesa is Swahili for money), which started in Kenya. People there use their phones to store cash and pay for goods. Similar solutions exist in many countries. Even in a place as remote and difficult as Somaliland, you can see these at work, as I did recently.

Madagascar is an island-country with incredible beauty and an abundance of things not seen across Africa, including natural resources, farmable land and water, not to mention lemurs. Yet the country is incredibly poor, with a countrywide per capita GDP of $400, which puts it in the bottom 10 countries of the world. On average, people live at the extreme poverty level of $1.25 per day in purchase power. One city I visited in Madagascar is home to the UN Millennium Development Goals, which is programmatically working to improve these extremely impoverished areas.

Sign signifying the entrance to a town in rural Madagascar designated a Millennium Development Goals location, one of about a dozen worldwide. Steven Sinofsky

Sign signifying the entrance to a town in rural Madagascar designated a Millennium Development Goals location, one of about a dozen worldwide. Steven Sinofsky

Yet technology is making a huge difference in lives there. Madagascar has three main mobile phone carriers. These are all prepay, and penetration is extremely high, even in the most remote areas. The country is wired with mostly 2G connectivity; there is some coverage at 3G, but it is highly variable. The only common use for 3G is for Internet access using external USB modems connected to PCs (usually netbooks) and shared.

Most of the phones in use are feature phones, often hand-me-downs from the developed market. I’ve even seen a few iPhone 3s. One person complained about being unable to update iOS because he has no high-speed connection for such a download (showing that people are connected to the world, just not at a high download speed). A developed-market smartphone is pretty much a feature phone here, and the cost of another network upgrade means that one is far off. People are anxious for more connectivity, but along with cost, the current state of government will make progress a bit slower than citizens would like.

A huge problem in this type of environment is safely dealing with money. Madagascar’s currency trades at $1 U.S. to 2,500 Madagascar ariary. When you live off of 3,000 or so a day, you’re not going to carry around three bills, so very quickly you end up with a brick of 100 Ar notes. What to do with all those? Where can you put them? How do you keep them safe? How can you even keep them dry in a rain forest?

Well, along comes mobile “banking.” As easy as you can recharge your phone, you can add money to your stored money account. You walk up to a kiosk — there are thousands and thousands of them — and in a series of text messages with the shopkeeper, you give her money and your phone gains stored value.

Home and storefront selling recharge minutes for pay-per-use mobile phones; also a station for mobile-phone banking in rural Madagascar. Steven Sinofsky

Home and storefront selling recharge minutes for pay-per-use mobile phones; also a station for mobile-phone banking in rural Madagascar. Steven Sinofsky

With iOS and Android fragmentation, how would these apps work, given what must be finite dev resources? The implementation of this is all through an old-school standard called SIM Apps or Sim Application Toolkit.

This set of APIs and capability allow the installation of apps that reside on your SIM. These apps are simple menu-driven apps that look like WAP sites. They are secure and controlled by carriers. Using this framework, mobile banking has reached unprecedented usage and importance in developing markets, particularly in Africa.

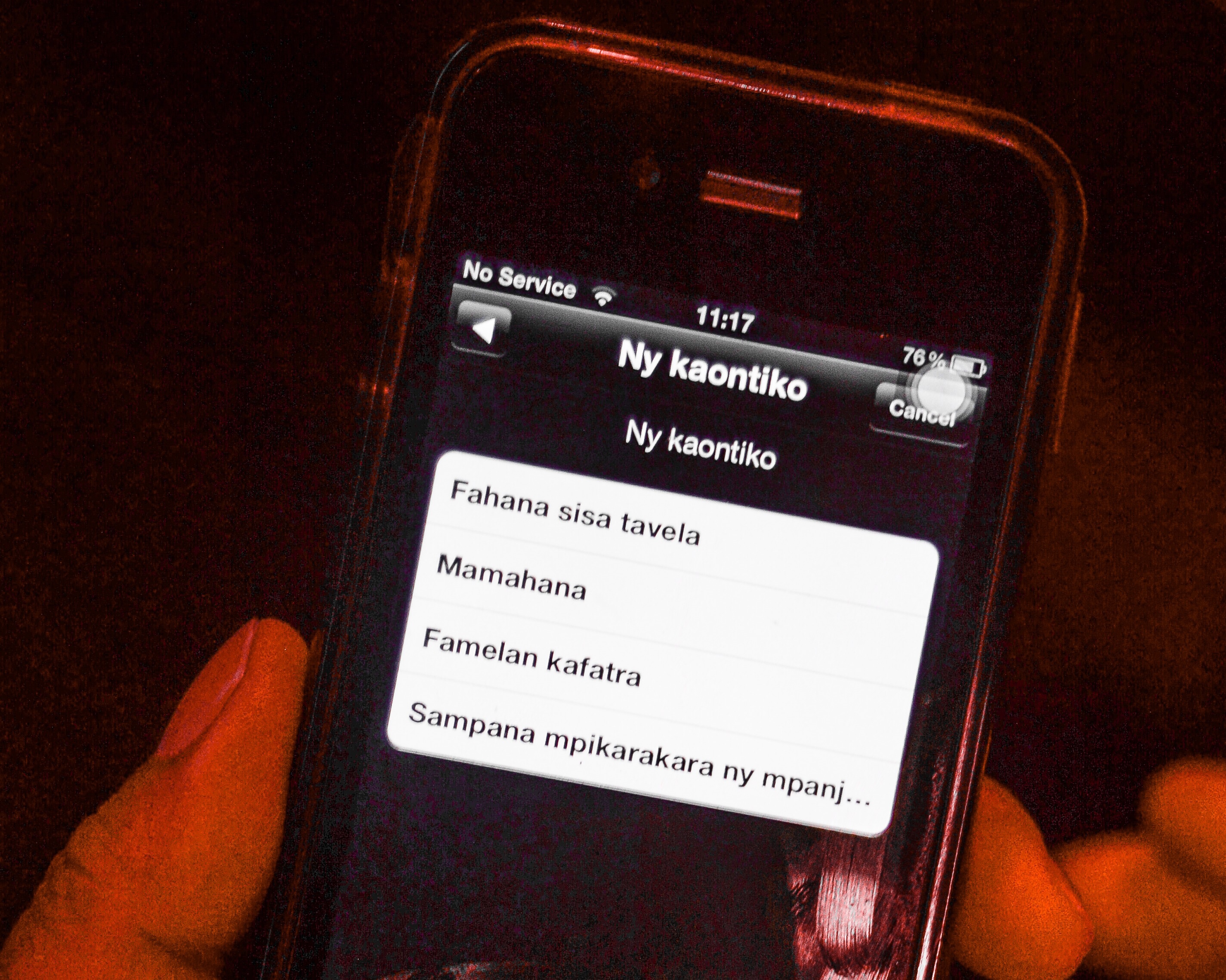

The scenario for usage is quite simple. You charge your phone with money, just as you would with minutes. When you want to buy something, you bring up the SMS app (pictured below, on an iPhone 3 in Malagasy) and initiate a transaction. The merchant gives you a code, which you enter along with the merchant’s identifying code. You then type in an amount, which is verified against your current balance. The merchant then receives a notification, and the transaction is complete. The whole system is safe from theft because of the connection to your mobile number, two-factor authentication and so on. There is no carrier dependency, so you can easily send/receive to any carrier, though the carrier has your balance. This isn’t an interest-earning savings account, but rather a transaction or debit account (of course, in the U.S., few of us earn interest on demand deposits these days, anyway).  Screen showing “My Account” in Malagasy, displayed on a recycled iPhone 3 (note the absence of a cellular connection). Steven Sinofsky

Screen showing “My Account” in Malagasy, displayed on a recycled iPhone 3 (note the absence of a cellular connection). Steven Sinofsky

You can also give and receive money from individuals. This is extraordinarily important, given how there can be distance between family or even the main wage-earning in a family. The idea of sending money around to family members is an incredibly important part of the cash economy of low-income people. This market, called “remittance,” is estimated to be over $400 billion in developing markets alone.

Life is easier and safer for those using mobile banking this way. You can count on your money being safe. You don’t need to carry around cash and worry about loss, theft, or water and weather destroying physical currency. You can easily deal with small and exact amounts. As a merchant, you don’t have to make change. It is just better in every dimension.

The carriers profit by taking a percentage of the transaction, which is high in the same way that check-cashing in the U.S. is high (and credit cards, for that matter). The fee is about two percent, which I am not sure will be sustainable, given the competition between carriers. I also think it will be fascinating to see how developed-market companies like Western Union evolve to support mobile payments, as they provide integration points to the developed-market financial systems. It is not uncommon to see a Western Union representative also offering phone recharge and mobile banking services.

In our environment, we would see this as a convenience, like a debit card. But in Africa, it is far more secure and convenient, because you only need your phone, which you will carry with you almost all the time, just as we do in the U.S.

I think the most interesting point of note in this solution is how it essentially skips over banking. If we think about our own lives, and especially those of the generation entering the workforce now, banking is most decidedly archaic. The whole idea of opening an account and dealing with a level of indirection which offers very little by way of useful services — it just feels like there’s a need for disruption. Our installed base of infrastructure makes this very difficult, but in the developing world that challenge doesn’t exist. It isn’t likely that most people will graduate to full-fledged banking just as we don’t expect people to graduate from a mobile phone to a full-fledged PC.

It also isn’t hard to imagine this type of mobile banking taking off first in the cash-based part of the developed world, where today people pay fees to cash checks and buy money orders, absent a bank account. The large numbers of check-cashing storefronts located near lower-income areas share much in common in some ways. One example is remittance. Many immigrants in the U.S. are the source for remittance funds going to developing markets. Seattle, for example, has one of the largest populations of Somalians outside of Northern Africa, and they routinely send funds back to their families. Today, this is a difficult process, and could be made a lot easier with a global and mobile solution.

Looking forward

Merchant using a credit-card reader attempting to get a stronger signal to complete the transaction in Anosibe, Madagascar. Steven Sinofsky

I look forward to solutions like this for our own lives here in the U.S. We see some of this in service-by-service cases. For example, using Lyft is completely cashless. I can use PayPal at merchants like Home Depot. Obviously, we all see Square and other payment mechanisms. Each of these shares a common connection to established banking and plastic cards. That’s where I think disruption awaits. Will this be bitcoin alone? Will someone, even a carrier, develop and scale a simple stored-value mechanism like that being used by billions of people already?

For myself, and no doubt for many reading this, this transformation is old hat. I’ve seen these changes over the past decade across many countries in Africa and elsewhere. Africa isn’t single-marketplace by any stretch. What is working in Madagascar, Kenya, Somaliland and others might not work elsewhere, or might not work for all segments of a given economy. Stay tuned for more observations from this trip.

It is always worth a reminder how some changes can bring about a massive difference in quality of life.

–Steven Sinofsky @stevesi

P.S.: What happens when you’re forced to use high-tech 3G connectivity to do a Visa card transaction? The merchant (pictured above) goes outside in a rain forest and aims for a stronger connection for the card reader. Yikes!